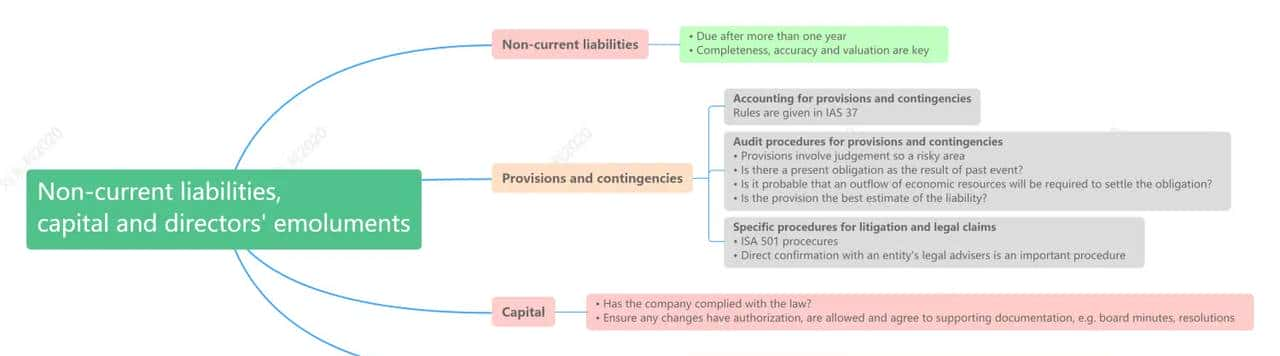

In this chapter, we begin with the audit of non-current liabilities and provisions. Questions on long-term liabilities such as long-term loans may be linked to other areas you have studied in the AA syllabus. For example, as part of a question on going concern you may be required to list procedures to audit the ability of the company to repay a long-term loan. Procedures detailed in this chapter will be relevant, for instance, confirming the terms of the loan to a loan agreement or evidence of whether any covenants exists.

The audit of provision is notoriously complex because of the degree of judgment used and the availability of the sufficient audit evidence. This is likely to be tested in a mini scenario question so you must be able to apply your knowledge to the question s circumstances. For example, you may be asked for the substantive audit procedures in respect of provision for legal claims.

The chapter ends looking at the audit of share capital, reserves and directors emoluments. Every type of liability covered in this chapter can form the basis of a constructed response question in the exam, in full or in part. The audit procedures and financial statements assertions can also be tested in the form of OT questions in section A or a longer section B question.

© 版权声明

文章版权归作者所有,未经允许请勿转载。

相关文章

暂无评论...